Janseva Co-operative Credit Society Ltd.

Registration No. :- MSCS / CR / 335 / 2010

Registration No. :- MSCS / CR / 335 / 2010

Society has its objective to provide best financial services to the society members.

Shares and deposit mobilization

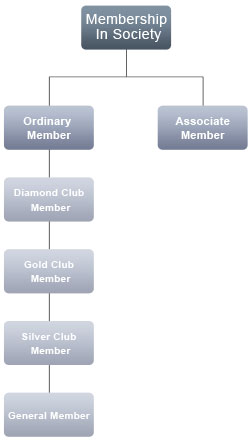

Society has decided to mobilise fund through share capital and various types of Deposits. If anyone wants to join society he/she should become the member of the Society. There are two categories of member’s namely ordinary member and associate memb

Eligibility for Membership

Any citizen of India, subscribing to the objectives, policy and programs of the society and competent to contract under Indian Contract Act 1872(9) having residence or occupation in operational areas of the society i.e. in the states of Andhra Pradesh, Bihar, Chhattisgarh, Delhi, Karnataka, Madhya Pradesh, Maharashtra, Orissa, Rajasthan, Tamil Nadu, Uttar Pradesh and West Bengal will be eligible to become member of the society.

Ordinary Member

An applicant will be enrolled as ordinary member of the society in accordance with clauses 9 and 10 of the bye laws of the society. Without prejudice to the provisions of the bye laws of the society, an individual, cooperative societies, government undertakings and SHG’s can apply for membership in a prescribed application form. For reasons of motivation and mobilization there will be four categories of ordinary members as below.

Diamond Club Members

Persons subscribing more than or equal to 5000 shares of the society worth Rs 100/- each, contribution 1% of the share amount i.e 5000, towards the membership processing charges and pay admission fee of Rs 10/- shall be classified ad Diamond Club member.

Gold Club Member

Persons subscribing more than or equal to 1000 shares of the society worth Rs 100/- each, contribution 1% of the share amount i.e 1000, towards the membership processing charges and paying Rs 10/- as admission fee shall be classified as Golden Club member

Silver Club Member

Persons subscribing 100 shares worth Rs 100/- each, contribution 1% of the share amount i.e, more towards the membership processing charges and pay Rs 10/- as admission fee will be termed as Silver club member.

General Member

Persons subscribing minimum 10 shares (as decided by the board) worth Rs 100/- each, contribution 1% of the share amount i.e 100 or minimum Rs. 100 whichever is more, towards the membership processing charges and pay Rs 10/- as admission fee will be termed as General member Associate Member The society in the interest of the people as well as promotion of its business may admit any eligible person as associate member on payment of a non refundable fee of Rs 10 or more as prescribed by the Board from time to time provided he/ she applies in prescribed application form and agrees to abide by the rules and regulations in currency and the decisions of the board from time to time. Types of Deposit Accounts

Demand Deposits

Term Deposits

Demand Deposits

Demand Deposits Demand deposits of different natures will be treated as qard e hasnah. Hence it will be the responsibility of the society to return the same to the depositors as and when demanded as per the policy and practice.

Amanah Compulsory Saving Deposit Account (ACSD)

In pursuance of the basic objective of promotion of thrift habit among the members, it has been decided that every ordinary and associate member shall have to open a compulsory savings deposit account to save minimum Rs 10 per day or Rs.250 per month. The lock in period of this account will ordinarily be two years. However amounts deposited over and above the minimum balance can be withdrawn any time as in the case of ACD. The society shall have right to utilize this amount at its own risk and return for the benefit of the society and its members. However, the depositors shall remain indemnified from outcome of fund utilization and hence returnable in full on demand. The amounts deposited shall continue to remain as Amanah Fund unless otherwise it is converted in any form of investment deposit account by the member after a year if they so desire.

Amanah Current Deposit Account (ACD)

Under this account, the deposits are held as Amanah, kept safe and secure, liquid and withdrawable in part / full any time. However the society shall have right to utilize it when idle at its own risk and cost. The depositor does not share in risk or return of the fund utilized in any form. Like current accounts of the banks, members can put their savings and withdraw the same at any time they desire. Hence such deposits will be free from any lock in condition with regards to deposits and withdrawals.

SHG Savings Deposit Account (SHGSD)

This is a special type of ACSD account. Each member SHG of the society shall have to save minimum Rs.1800 /- pm, (i.e. Rs 4 (+1 membership fees) per day or Rs 120 (+30 membership fee) per month and deposit the same on daily or monthly basis), for a period of three years. Amounts so deposited shall in the successive years become eligible/ entitled for investment and hence profit subject to the option/approval of respective SHG.

Mutual Help Fund Deposit Account (MHFD)

This account may be opened by a group of members of the society engaged in trade, commerce and industry. This is a joint liability group account where minimum 5 and maximum 20 members will come together and open MHFD account. Each member will contribute an equal sum and avail interest free loan facility every month equivalent to the total monthly deposit. A lottery or mutual agreement among the members will decide the beneficiary of this loan month after month. The loan advanced under this scheme will be a joint liability of members of MHFD and society shall remain indemnified for any kind of loss whatsoever. Members of this group, as an alternate of monthly loan facility, may avail overdraft facility against trade bills with a maximum limit of Rs. 1 to 5 lakhs as guaranteed by the group and decided by the Area Managing Board from time to time. The society may charge fees equivalent to half/one percent of the loan amount/overdraft or other fees as decided by Area managing Board from time to time as scheme management and maintenance fee.

Service/Support Recurring Deposit account (SSRD)

Deposits from the members may be accepted for making themselves eligible for availing regular support services to them, their families/relatives and others on monthly basis. For instance, payment of electricity bill, telephone bills, supply of domestic goods and transfer of funds etc as per the prescribed rule of the society. The account holders may avail service charge free overdraft/ credit facility for a maximum period of 25 days or the last day of the month in which this facility is availed, whichever is earlier. In case of failure to pay within stipulated period, the overdraft will be treated as general loan and hence service charge as per the current practice will be levied accordingly. The amount of overdraft may be up to five times of the recurring deposit or balance maintained, as the case may be with a maximum limit of Rs 5000/-only. . Minimum average balance to be maintained in ACD accounts may be Rs.100, ACSD shall be @ Rs 250, SHGSD account shall be @ Rs 1500 per month on the regular basis and MHFD shall be equivalent to one month’s fund or otherwise as may be decided by the board from time to time.

Term Deposits

Term deposits are primarily investment deposits of various natures. Members desirous to avail investment facility provided by the society may open this account in addition to ACSD or any other accounts. These depositors shall have to submit a declaration that they want their monies to be invested in a manner free from interest, speculation and gambling (Shariah compliant manner). Further that they indemnify the society for any kind of loss of profit or capital or both that may occur in the process of investment exercise. The amount received under these accounts will be invested on profit loss sharing (PLS) basis in various kinds of income generating sources / avenues / businesses as per the decision of the board of directors on recommendation or in consultation with Business Promotion Cell (BPC) of the society. Wherever possible consent of the depositors/investors shall be obtained before investment of funds. These investment accounts may be of various types as described below or as may be modified by the board from time to time.

Recurring Investment Deposit Account (RID)

On desire or instruction of the members, amount saved in ACSD, ACD and SHGSD completing one year, may be transferred in RID account. Such amounts will be invested in business preferably leasing and therefore become eligible for risk and return in form of profit. The lock in period for such accounts will be minimum 3 years and maximum five years or as the nature/ period of investment may be.

SHG Corpus Fund Deposit Account (SHGCFD)

This is a special purpose account to provide Qard-e-hasnah to poor especially SHG’s or its members out of social responsibility to the poorer sections of the society. Philanthropists/donors of the community/organisations may be requested to come forward to discharge their social responsibility and open this account with an amount of Rs 6000/- (inclusive of grant component of Rs 1000). The amount of Rs 5000 deposited in the account shall be in form of SHG Corpus fund. This amount will be advanced to preferably SHGs or their members as qard e hasnah. The loan amount returned back may become part of revolving fund or if conditioned shall be returned back to the depositors. In case of conditional corpus deposit, the account holders shall have the right to take back Rs 5000 after the period of three years provided Qard-e-hasnah advance is received turned back by the society from the beneficiaries. The Amount deposited in this type of account will not be a liability of the society. Depositor shall have to indemnify the society from the loss of the SHGCD amount if the same is lost in the loan process.

Asset Based Investment Deposit Account (ABID)

Deposits received under this head shall be invested in ETF (exchange traded fund/Gold/silver or any other metal or other assets like land, building and machinery (based on Murabaha, Ijara or other mode as the case may be) in assets which are likely to earn fixed rent or return.

Portfolio Investment Deposit Account (PID)

Deposits received under this account will be invested in the equity shares of the companies/corporations/government and semi government undertakings listed in stock/capital and commodity markets, as decided by the BDC of the society.

Participatory Business Investment Deposit Account (PBID)

Deposits received under this account may be invested based on PLS system (Musharka) in businesses specially society’s Service and Support Schemes.

General Investment deposit Account (GID)

Deposits received under this account for investment without any pre condition will be used in any venture which ensures reasonably good return and generates employment and self employment avenues for the members of the family.

SPV Investment Deposit Account (SPVID)

Investment may be invited and accepted under this account for specific purposes as notified by the society from time to time. Specific purposes may be investment in the purchase of land for housing purposes, development of housing society, industrial houses, society’s offices, conference room and guest houses and alike in the interest of the members and the society.

The minimum investments in various kinds of schemes will be decided by the society from time to time.

Security Deposit Account (SD)

Security amount/ caution money collected by the society for enabling people or members to receive specific facilities provided by the society shall be accepted and put under this category of deposits. It will be an amanat and shall be returned to the depositor as per terms agreed by and between the parties.

Honouring withdrawals

We understand the need of members, so withdrawals are all time available to members. Depending on the type of accounts held in JANSEVA, you can generally withdraw any amount from the JANSEVA at any branch office, with no extra charges. However, you cannot withdrawals more than your account’s amount (depends types of account you have).

Loan and Financing

Members of the society can avail the loan and debt financing facility by the society as per the term and condition of the Society.

Interest Free Loan:

Funds mobilized from ACSD and other idle funds, interest free loans will be advanced to the members on the in various categories of loan. On decided terms and conditions or as decided by the Board from time to time.

Categories of loan in order of priority

Debt Financing:

Funds mobilized from special accounts and other idle funds. Debt financing facility will be provided to the members on decided terms and conditions or as decided by the Board from time to time.

Eligibility for Loan

Members desirous to avail loan facility shall have to apply in a prescribed loan application form subject to the condition that they hold shares of the society worth minimum 2.5% value of loan in case of secured loan and 5% value of the unsecured loan applied.

Registered Office

AICMEU 1st Floor, Vazir BuildingAdmin Office

Janseva Cooperative Credit Society Ltd, 7/25 A 2nd Floor Grant building Arthur Bunder Road,